admin

Comments

-

TT claims are used as the exposure base for the lower frequency, higher severity injury types. Frequency is measured by per $100 of payroll and severity backed into. All raw frequencies and severities by injury type are converted into relativitie…

-

A key idea of Couret & Venter's paper is the TT counts serve as an exposure base for the lower frequency but higher severity accidents. This is why we measure everything relative to TT claims because we can then scale.

You have the set …

-

Yes, use the one which is closest in absolute value. There isn't a restriction about going over or being under.

-

We reviewed the Fisher source material; on page 40 (46 in the PDF), footnote 19 says "If a retro policy also has a per claim loss-limit, the charge for that is sometimes considered part of the insurance charge, and sometimes cons…

-

As you say, a continuous approximation model isn't really defined anywhere in the source material. The closest the source comes is mentioning that applying Panjer's algorithm is an example of a collective risk model.

In Panjer's algorithm w…

-

A driver with 0 accident free years has had at least one claim in the last year. Suppose there are N such drivers in this group. A key assumption of Bailey & Simon is the observed claim frequency, lambda, for the class is the same for all sub…

-

The graph is hard to read; different sample answers use different 1-in-100 year PMLs. I'll assume the 1-in-100 year PML is $100 million.

With a 20% quota share the ceded premium is 0.2*50m = 10million.

The terms of the quota share tre…

-

Here's a hint: The excess ratio is (E[X] - E[X; xi]) / E[X]. For a uniform distribution on [0, 10], E[X] = 5 so we just need to find an expression for E[X; xi].

SPOILER: If you're still stuck, see the picture below…

-

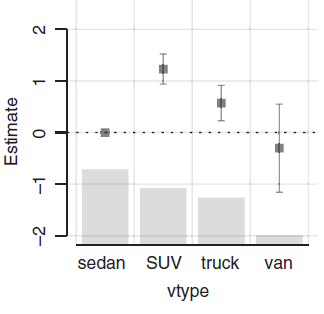

Let's formulate the GLM output using our figures:

Estimate (ignore std error and p-value for now)

(Intercept) c

EngineSize:small …

-

It doesn't call out the term power law explicitly. It's assumed that AOI^k where k is a constant and AOI is the variable of interest is recognized as an example of a power law.

If the residual plot showed something looking like exponential …

-

The battlecard is correct. In this case, the GLM output would contain a separate entry for EngineSize: Small, say -0.300, and suppose the EngineSize: Small; BodyType: Van coefficient is -0.250.

In absolute terms we have some base class for…

-

In the interacting two categorical variables example we have the sprinkler discount for class two requires two GLM coefficients to calculate it (sprinklered coefficient, and the occupancy class 2: sprinklered yes coefficient). The same is true fo…

-

In general if you are using a log link function then you should log your continuous variables. The max(log(age)-25,0) comment is because the age variable is not logged in this partial residual plot so the hinge point is placed at an unhelpful loc…

-

Typo fixed - most = more.

Since the per-occurrence limit is hit more frequently than the aggregate limit we have more data available for pricing it. It's generally advisable to update/refresh rating factors once you have sufficient data rat…

-

I don't think it's possible to write down a general approach here. It would involve undoing the link function and depends on whether the scale of the variable used in the hinge function matches the scale of the link function. Broadly speaking, if…

-

The retro premium consists of the basic premium plus the converted ratable losses, all multiplied by the tax multiplier. The ratable losses are the insured's actual experience within the bounds of the per-occurrence and/or aggregate limits/deduct…

-

Your expression for Var(S) is incorrect, it violates the law of total variance. The correct formula is the compound variance formula https://e…

-

Here's an example from p.15 of the GLM text.

It is the original predictor which increases at an increasing rate. The target variable will also increase at an increasing rate with respect to that particular original predictor but its overall response will be determined by net effect of all t…

Yes, you are correct in both cases.

The NCCI circular uses a slightly different but equivalent presentation of the balance equations. The tax multiplier is included implicitly via lines 12 and 13 which are used in 14 and 15.

You can rewrite the Fisher balance equations by mu…

Employers and people are sensitive to price changes. If you're going to receive less of a price increase for reporting a loss then you're more likely to report it and let the insurer handle the claim for you. Any time your premiums go up, you're …

Remember the NCCI experience plan is a split-loss plan so responds to frequency as well as severity. Assuming the expected loss used in rating is accurate and we're just dealing with an underreporting of med claims, the ballast (B), weight (W) an…

Let's take the example of a Collision deductible. Suppose you offer $500, $1,000 and $2,000 options for the deductible. Logically, as you increase the insured's deductible they should pay less as we assume the expected loss is unchanged so the in…

Thanks for pointing this out. You're correct.

Change claim number 4 to be N with 52% predicted probability of going to litigation and you get what we were aiming to show. We're updating the files now.

When an employer reports claims it causes their premiums to go up because the experience mod increases. The mod is determined by the mix of claim types. If there is less weight on the med-only then those claims have less influence on the mod so t…

I could be wrong but in my opinion price optimization isn't occurring here. Price optimization would be if we had two insureds with identical rating characteristics that receive different rate changes based on our expectation of the likelihood of…

Yes, building a GLM is an iterative process. You start by assuming a target variable distribution such as a gamma distribution, build the GLM and then look at the deviance residuals to assess if your choice was appropriate. If the deviance residu…

I think I see where you're coming from. There is ambiguity about what we're defining here as an exposure. In a pure premium model the response variable we're looking at loss $ / earned house years but in a severity model we're looking at loss $ /…

In our opinion, this exam question is ambiguous because it doesn't tell you what type of table of insurance charges you're given. Is it a limited table M or a regular table M?

The sample 1 solution assumes it is a regular table M and we're …